A Collapse at the Reading Terminal

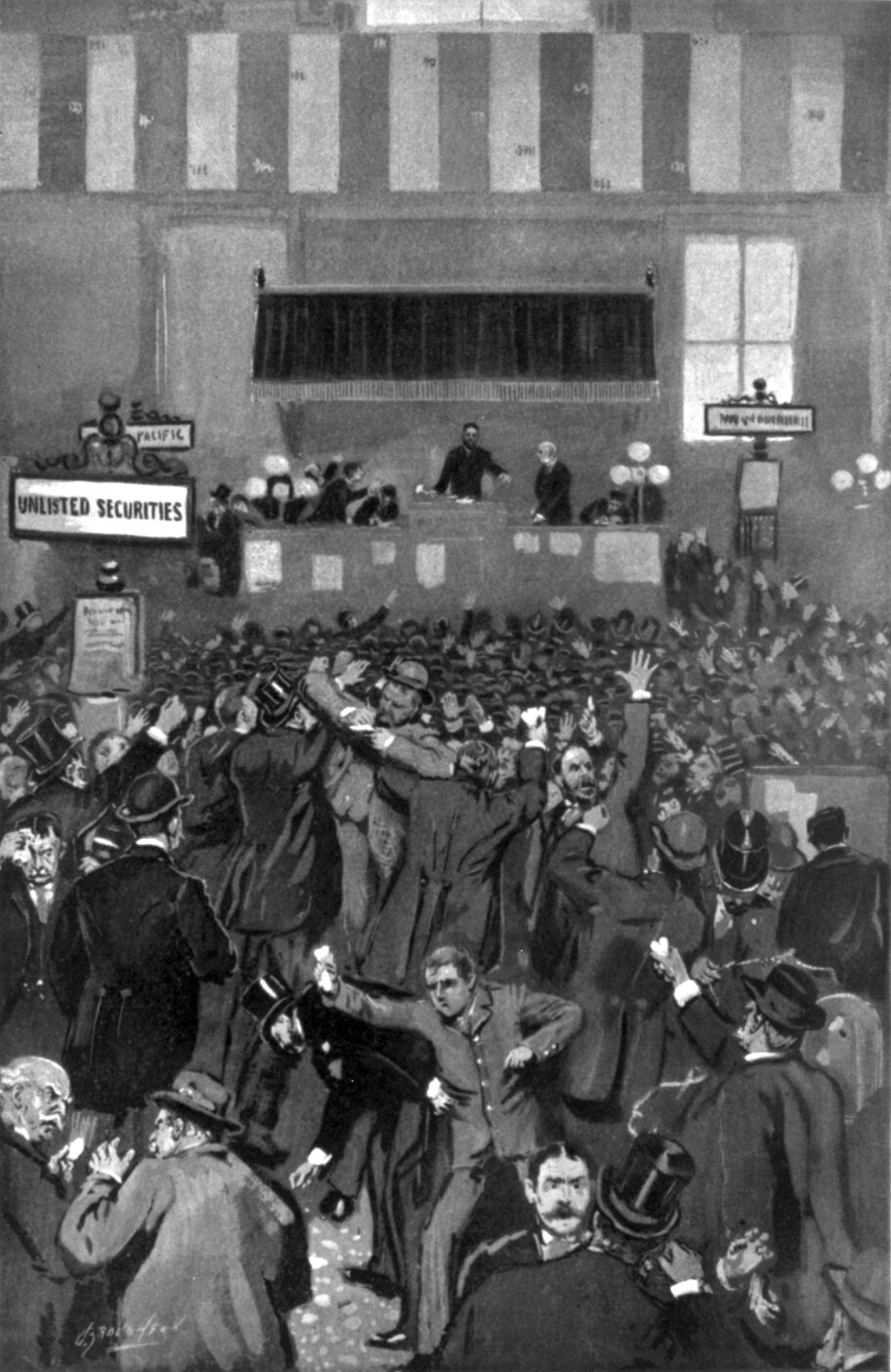

On the morning of February 20, 1893 — ten days before Grover Cleveland's second inauguration — the directors of the Philadelphia & Reading Railroad filed for receivership in a Pennsylvania courtroom. The company carried $125 million of funded debt, more than the federal government's annual revenue, and its president had just confessed that interest payments could not be met. Wall Street, reading the morning papers, marked Reading common down sixteen points in an hour. A month later the Erie cut its dividend. Ten weeks after that the National Cordage Company — one of the great rope trusts of the industrial age, capitalised at $20 million and trading above par just weeks earlier — went into the hands of receivers on May 5. Cordage had been the most widely held speculative stock in New York. When it cracked, the whole market cracked with it.

Within ninety days of the Cordage collapse, 128 national banks had suspended payments, dozens of state banks and loan companies had closed their doors, and the unemployment rate had begun the climb that would carry it past 18 percent by the winter of 1894 (Romer, 1986). The Panic of 1893 was not the worst panic in American history measured by a single bad week — that honour arguably belongs to 1907 or 1929 — but the depression it unleashed was, until the 1930s, the longest and most grinding the republic had ever seen. It destroyed one Democratic administration, reshaped both political parties, and ended with the dollar bolted to gold for a generation.

The Sherman Act and the Silver Leak

The machinery of the disaster had been assembled three years earlier. In July 1890 Congress passed the Sherman Silver Purchase Act — a political compromise that gave western silver senators what they wanted (a government bid for their metal) in exchange for eastern protectionist votes on the McKinley Tariff. The law required the Treasury to buy 4.5 million ounces of silver every month — roughly the entire output of the American mines — and to pay for the metal with new Treasury notes of 1890, redeemable on demand in "coin." The Treasury interpreted "coin" to mean gold, because that was the only way the notes would circulate at par. Silver at the legal ratio of 16 ounces to 1 ounce of gold was worth about $1.29 an ounce at the mint; the world market price was already under $1.05 and falling.

The arbitrage was irresistible. Anyone holding a Treasury note could present it at the Subtreasury in New York, take out gold, export the gold to London where it bought more silver than the American mint gave for it, and repeat. The Treasury's gold reserve — the notional backing for more than $346 million of Civil War greenbacks as well as the new silver-era notes — began to leak out through the same redemption window that Jay Cooke's bondholders had used a generation earlier. By the end of April 1893 the reserve had slipped below $100 million for the first time since resumption in 1879, breaking a psychological floor that both political parties had treated as sacrosanct (Friedman and Schwartz, 1963).

Railroads Built Beyond the Continent

If the silver law was the slow leak, the railroads were the dry timber. American rail mileage had doubled between 1878 and 1893, from roughly 87,000 route-miles to more than 170,000 — a network already larger than all of Europe's combined and still expanding into territory that could not possibly generate freight to service the bonds. Much of that construction had been financed in London, Amsterdam, Frankfurt, and Paris. European savers took the paper on faith because American railroad bonds had paid reliably for two decades. When Baring Brothers nearly failed in November 1890 on the back of bad Argentine debt, that faith evaporated overnight. The Bank of England doubled its discount rate, the Rothschilds organised a guarantee fund, and European capital began flowing out of every emerging market it could reach — including the American West. The crisis is covered in detail in our companion piece on the Baring crisis of 1890.

By 1892 the overbuilt trunk lines were competing themselves to the edge of solvency. Freight rates had fallen by roughly a third in a decade. The Reading had borrowed heavily to buy up anthracite coal lands and assemble a de facto monopoly on Pennsylvania's hard-coal output; when the monopoly broke on an Interstate Commerce Commission ruling, its bondholders found they had lent against assets that could no longer carry their coupon. Interest came due on February 15. The Reading went down five days later.

The receivership wave of 1893–1894 took out a substantial share of the American rail network. By the end of 1894 roughly a quarter of total mileage was operating under court-appointed trustees.

| Railroad | Receivership | Route miles | Outcome |

|---|---|---|---|

| Philadelphia & Reading | February 1893 | ~2,100 | Reorganised 1896 under J.P. Morgan plan |

| Erie Railroad | July 1893 | ~2,000 | Reorganised 1895 as Erie Railroad Co. |

| Northern Pacific | August 1893 | ~4,700 | Reorganised 1896 under Morgan plan |

| Union Pacific | October 1893 | ~7,500 | Reorganised 1897, Harriman took control 1898 |

| Atchison, Topeka & Santa Fe | December 1893 | ~9,300 | Reorganised 1895 as AT&SF Railway |

The reorganisations that followed were as consequential as the failures themselves. J.P. Morgan's firm — working beside Kuhn, Loeb on the Union Pacific — ran most of them on a model he would export to the rest of the industrial economy: wipe out common equity, cut bond coupons, install voting trusts, and put a banker on every board. By 1900 "Morganisation" controlled a third of the nation's rail mileage.

Summer of Broken Banks

The specific shock that turned a Wall Street sell-off into a general banking panic arrived in late June. New York's clearinghouse banks, watching their gold reserves fall, began refusing to clear cheques drawn on interior correspondents. Country banks in turn suspended cash payments to depositors, and by mid-July "currency famine" had taken hold across the Midwest and South. Currency traded at a premium of 2 to 4 percent over certified cheques — a physical scarcity of money, not merely a credit crunch. Clearinghouses from Cincinnati to Atlanta issued their own substitute "clearinghouse certificates" in denominations as small as one dollar to keep payroll moving (Sprague, 1910).

The banking casualty list ran longer than any previous American panic. Over the course of 1893, some 360 state banks, 158 national banks, and 172 private banks, trust companies, and savings institutions suspended — nearly 700 suspensions in all, a figure the country would not see again until 1929. Business failures for the year exceeded 15,000; the following year added another 14,000. Mercantile agency R.G. Dun, in its 1894 annual circular, noted the "two fiscal years of stress through which no previous period of industrial prosperity has been so sharply broken" (Noyes, 1909). The wholesale price index, already soft, fell an average of 2.5 percent per year between 1893 and 1896, deepening the real burden of every fixed debt contracted during the boom. For the dynamics of that persistent deflationary environment, see our fuller treatment of the Long Depression of 1873–1896.

Cleveland Goes to War With His Own Party

Grover Cleveland had been elected on a gold-standard Democratic platform in November 1892, and he regarded the Sherman Silver Purchase Act as the immediate cause of the gold outflow. On June 30, 1893, he called Congress into special session for August 7 with a message that left no doubt where he stood:

"The people of the United States are entitled to a sound and stable currency and to money recognised as such on every exchange and in every market of the world. Their Government has no right to injure them by financial experiments opposed to the policy and practice of other civilized states."

The repeal fight consumed the late summer. In the Senate, silver Democrats led by John P. Jones of Nevada and William Stewart filibustered for seven weeks. Cleveland's postmaster general reportedly threatened to withhold patronage from any Democrat voting against the bill. On October 30, 1893, the Senate repealed the silver purchase clause by 43 votes to 32; the House had already done so in August, 239 to 108. The Democratic party split that opened during the debate would not close again until the 1930s.

Source: Noyes, Forty Years of American Finance (1909); US Treasury Daily Statements

The chart tells the monetary story as cleanly as any narrative. Every time the reserve approached $100 million, another bond issue or a Morgan-led syndicate pulled it back. Every few months the drain resumed.

Coxey's Army and the Pullman Strike

Repeal did not end the depression. Through the winter of 1893–1894, unemployment rose in every industrial city. Jacob Coxey, a Populist quarry owner from Massillon, Ohio, proposed a $500 million federal public-works bond issue to be spent on rural road construction — an idea forty years ahead of its time. When Congress ignored the proposal, Coxey led a march of roughly 500 unemployed men on Washington in April and May 1894. They arrived at the Capitol steps on May 1. Coxey was arrested for walking on the lawn. His march drew dozens of imitator "armies" from the West and Midwest, most of which commandeered freight trains to travel east. It was the first mass march on Washington in American history.

A month later George Pullman cut the wages at his company town south of Chicago by nearly a third without cutting rents in the Pullman-owned worker housing. The American Railway Union, under Eugene Debs, called a sympathy strike that by early July had halted most rail traffic west of Chicago. Cleveland broke the strike with federal troops over the objection of Illinois governor John Peter Altgeld, invoking the interstate mails and the Sherman Antitrust Act — the same law that had been enacted to break corporate monopolies, now deployed against a labour union. The Pullman strike radicalised Debs and pushed an entire generation of industrial workers toward the Socialist Party and the Populist coalition.

The Morgan–Belmont Rescue

By early February 1895 the Treasury's gold reserve had fallen to $42 million, and the daily drain was running at roughly $2 million. On February 5, Cleveland met in the Red Room of the White House with J.P. Morgan and August Belmont Jr., who represented the Rothschilds' American agency. Morgan proposed that his firm and the Rothschilds — through Belmont — organise a private syndicate to supply the Treasury with 3.5 million ounces of gold, about half drawn from European markets, in exchange for a new 30-year bond issue at 3.75 percent. The syndicate would guarantee that no gold deposited under the contract would be withdrawn through the redemption window. The face value of the bond issue was $62.3 million.

Morgan's biographer records the moment Cleveland hesitated over the legality of a private syndicate bond sale. Morgan pulled a copy of the Revised Statutes of the United States from his pocket, turned to Section 3700, and read aloud the provision authorising the Secretary of the Treasury to purchase coin with the proceeds of bonds. "That," he said, "is your authority" (Strouse, 1999). The contract was signed on February 8, 1895. The syndicate priced the bonds to the public at 112.25 within days, earning an immediate profit of several million dollars that became a political liability for the rest of Cleveland's term. Gold reserves held above $100 million for the remainder of his administration.

Rockoff (1990) has argued — drawing on Bryan's speeches, Baum's fiction, and the mint ratios of 1896 — that the whole silver debate lived on in popular memory through The Wizard of Oz, whose yellow brick road, silver slippers (changed to ruby in the film), and green Emerald City read as a coded allegory of the free-silver cause. Whether Baum intended the reading or not, the substrate he drew on was real.

Bryan's Cross of Gold

The political reckoning came in the summer of 1896. At the Democratic convention in Chicago on July 9, a 36-year-old former congressman from Nebraska took the rostrum to defend the free coinage of silver at 16 to 1. William Jennings Bryan spoke for 30 minutes with no prepared text and closed with the sentence that would define American politics for the next four years:

"You shall not press down upon the brow of labor this crown of thorns. You shall not crucify mankind upon a cross of gold."

The hall held still for something between ten seconds and a full minute — accounts vary — and then erupted. Bryan won the nomination on the fifth ballot the next day at the age of 36, still the youngest major-party presidential nominee in American history. He then campaigned across 27 states, travelled some 18,000 miles by rail, and gave more than 600 speeches to roughly five million people. William McKinley, his Republican opponent, stayed on his front porch in Canton, Ohio, while campaign manager Mark Hanna raised $3.5 million from corporate donors — a sum no previous campaign had approached — against Bryan's roughly $300,000. McKinley carried the industrial North and the urban East and won 271 electoral votes to 176.

The Gold Standard Locks In

The new administration moved to consolidate the monetary settlement. The Gold Standard Act of March 14, 1900 fixed the dollar at 25.8 grains of gold nine-tenths fine — the same ratio in force since 1837 — and formally withdrew silver as a standard of value. By 1900, gold discoveries in the Klondike (1896), Western Australia (1893), and the Witwatersrand (ramping from 1886) had expanded world gold output to a level that gave the depressed American economy the monetary expansion that silver advocates had demanded. Wholesale prices, falling for twenty-three years, turned and rose.

The political realignment of 1896 proved more durable than the monetary one. Republicans held the presidency for 28 of the next 36 years. The Democratic party carried Bryan's farmer–silver–labour coalition through two more losing Bryan campaigns before emerging, in Woodrow Wilson, with a different coalition and a different programme — one that included a central bank. The creation of the Federal Reserve in 1913 grew directly from the banking fragility the 1893 panic had exposed; the story of how that institution was assembled is told in the founding of the Federal Reserve. The Panic of 1907, when Morgan again rescued the Treasury in his library, was the event that finally broke the political resistance.

What 1893 Actually Settled

The Panic of 1893 settled three arguments and left a fourth open. It settled the currency question for 37 years — not in favour of gold as a matter of intellectual conviction, but in favour of whichever metal was expanding fastest. It settled the railroad question by transferring the industry's financial control from promoters and speculators to a handful of Wall Street houses led by Morgan. It settled, for the moment, the political viability of the free-silver coalition by allowing gold discoveries in South Africa and the Yukon to make the argument moot.

What it left open was the question of whether the United States should have a central bank, and on what terms. Cleveland had relied on a private syndicate because no public institution existed that could do the job; Morgan had rescued the Treasury because no public institution existed that could have refused him. Within twenty years, the country would answer that question. The answer it chose — a system of twelve regional reserve banks jointly owned by member banks but governed by a board appointed in Washington — was not the central bank the Populists had fought for, nor quite the one Morgan had designed. It was the central bank that a country embarrassed by both men decided it could live with.

By the time Cleveland left the White House in March 1897, the Treasury gold reserve stood at $140 million and rising. He left behind a ruined party, a reshaped railroad system, a new Republican governing majority, and the ghost of William Jennings Bryan's voice in the back of the hall, still promising that someone, someday, would not be crucified on the cross of gold.

Related

Historical records Learn more about our methodology.