A Bank Run in a City Built on Copper

On a cold morning in the autumn of 1664, depositors began arriving at the Stockholms Banco's premises near the Royal Palace, demanding redemption of their kreditivsedlar — the printed promissory notes that the bank had been issuing for three years and which had circulated through Sweden's commercial life with growing enthusiasm. The notes were supposed to be exchangeable on demand for the heavy copper plate money that anchored the Swedish currency. The bank had once boasted that any holder could walk in and walk out with copper. By autumn 1664, this was no longer true.

Johan Palmstruch, the bank's founder and a former Riga merchant, watched the queues lengthen with mounting dread. He had built his bank on a clever idea — that a piece of printed paper, signed and authenticated, could substitute for the awkward copper plates Sweden had used as money since the early seventeenth century. He had not built it to survive a run. The notes outstanding far exceeded the copper in the vaults, and Palmstruch knew it. So did the men in the queue.

What followed over the next four years was a slow, painful unwinding that destroyed Europe's most innovative bank, sent its founder to prison under sentence of death, and forced the Swedish Riksdag to do something no parliament had ever done. In September 1668, the four estates of the Riksdag chartered a successor institution placed deliberately under their authority rather than the king's. They called it Riksens Ständers Bank — the Bank of the Estates of the Realm. Three centuries later, that institution would be renamed Sveriges Riksbank. It has operated continuously ever since, and it is now the oldest central bank in the world.

Sweden's Copper Problem

To understand why Stockholms Banco existed at all, you have to understand the strange currency system of seventeenth-century Sweden. The Swedish empire under Gustavus Adolphus and his daughter Christina was at the height of its imperial reach — a Baltic great power whose armies had marched through Germany during the Thirty Years' War, whose territory included present-day Finland, much of the Baltic coast, and significant German possessions, and whose treasury was unusually dependent on a single export commodity.

That commodity was copper. The Falun mine in central Sweden was the largest copper producer in seventeenth-century Europe, supplying perhaps two-thirds of total European output at the peak of its productivity. Copper revenues funded the Swedish state, paid the army, and underwrote imperial ambitions. The fiscal logic was sound enough — a state should monetize what it produces — but the monetary logic produced an extraordinary side effect. To keep copper prices high, the Swedish Crown had begun in the 1620s to issue large copper plates as currency, denominated by weight against silver. A 10-daler plate weighed roughly 19 kilograms. A 4-daler plate, which Eli Heckscher described as "the most inconvenient currency ever introduced by a major European state," weighed about 7 kilograms (Heckscher, 1934).

These plates, called plåtmynt, circulated as legal tender for large transactions. Merchants moved them on horse-drawn carts. A wealthy purchaser of land in Stockholm might arrive with a wagon of copper as payment. The system was protected by import tariffs and royal decree, and it worked, in the limited sense that it kept Falun's copper bid up. As a money, it was barely usable.

The opportunity for innovation was obvious. If a trustworthy institution could accept the copper plates on deposit and issue lighter, more portable claims against them, the Swedish economy would gain an enormous practical benefit. This was the proposal Johan Palmstruch brought to the regency government of the young Charles XI in the early 1650s, and which Queen Christina's regents — Christina herself had abdicated in 1654 — granted by royal charter in November 1656.

Palmstruch's Two Departments

Stockholms Banco opened for business in July 1657. Palmstruch, a Riga-born merchant of Dutch ancestry who had spent time in Amsterdam studying its Wisselbank, organised the bank along lines that drew on but adapted the Dutch model. The bank had two departments. A Vexel-Banco, modelled on the Wisselbank, accepted deposits and provided clearing services for merchants. A separate Lähne-Banco — the lending department — extended credit. The two were supposed to be kept strictly distinct. They were not.

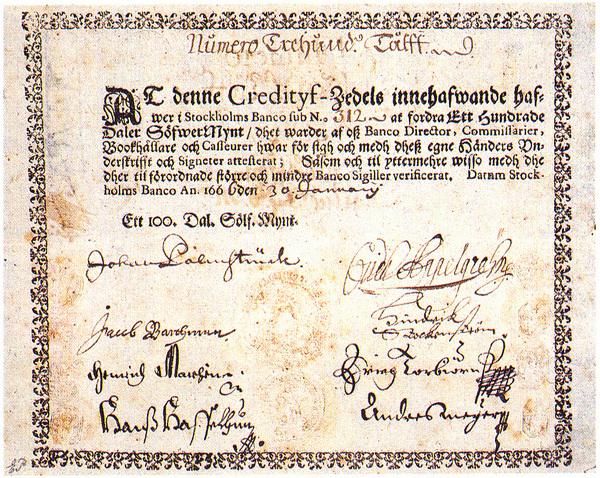

Palmstruch's most celebrated innovation appeared in 1661. To address the practical inconvenience of clients having to handle the copper plates physically when withdrawing their deposits, the bank began issuing kreditivsedlar — printed notes denominated in daler, signed by bank officers, and promising to pay the bearer the corresponding sum in copper or silver coin on demand. Earlier banks had used handwritten receipts and book entries. Palmstruch's notes were standardised, printed in fixed denominations, and designed to circulate hand to hand. Roberds and Velde describe these as "the first true banknotes in Europe — paper money in the modern sense, anonymous and transferable, indistinguishable in function from what would later become the standard form of currency" (Roberds and Velde, 2014).

The notes were popular. They displaced the heavy copper plates in everyday commerce almost immediately, and within a few years they were the preferred medium for large payments in Stockholm and beyond. The bank's profitability came from the spread between the interest it earned on loans and the zero interest it paid on the notes outstanding. As long as the notes circulated and were not redeemed, the bank earned this spread on the entire issue.

This was where the trouble began.

Royal Pressure and Over-Issuance

The young Charles XI had inherited the throne in 1660 at age four. Real authority rested with a regency dominated by the powerful Oxenstierna family and other noble factions. The regents needed money. The Treaty of Oliva had ended Sweden's exhausting war with Poland in 1660, but military expenditure remained heavy, the Crown was deeply indebted from earlier campaigns, and the political imperative to maintain Sweden's great-power posture was constant. Stockholms Banco, with its profitable capacity to issue paper money, became an irresistible target.

From 1663 onward, the bank was directed — formally and informally — to lend to the Crown and to politically connected nobles on terms that bore no relationship to commercial reality. Loans were extended to mining ventures, to military suppliers, and to Crown finances itself, often at interest rates well below market. The notes financing these loans flowed out into the economy. The copper backing did not keep pace.

By 1664, the imbalance had become acute. The bank had issued kreditivsedlar with face value substantially exceeding the copper held in reserve — Wetterberg estimates the ratio of notes to reserves at perhaps three or four to one by the mid-1660s, though the exact figures are contested because Palmstruch's bookkeeping was, as the eventual prosecution would establish, deficient (Wetterberg, 2009). What is certain is that when silver imports from continental Europe slowed in the mid-1660s — silver was needed to maintain confidence in the daler against the copper standard — the bank could not meet redemption demand.

The chart traces the silver content of the daler across the second half of the seventeenth century, drawn from Heckscher's reconstruction of Swedish monetary data. The decline from roughly 25.7 grams in 1640 to a low near 18.8 grams in 1668 captures the stresses on Swedish coinage that produced the Stockholms Banco crisis. After the Riksbank's establishment, the line stabilises and slowly recovers — partly because the new institution was constrained from over-issuance by parliamentary oversight, partly because Sweden's broader monetary policy was put on a more disciplined footing.

The Run, the Collapse, and the Trial

The first serious run came in autumn 1664. Word had spread that the bank was issuing notes far in excess of its reserves. Depositors who had been content to hold paper for the convenience of it began to want copper instead. Palmstruch responded by pleading with note-holders to be patient, by arranging emergency copper shipments from Falun, and by calling in loans — which proved largely uncollectible because they had been extended to the Crown and to noble borrowers who had no intention of repaying on schedule.

A second, deeper run came in 1667. By then the bank's insolvency was an open secret in Stockholm commercial circles. Notes traded at substantial discounts to face value. The Crown, embarrassed by the failure of an institution it had encouraged and exploited, began to look for a way to cut its losses without admitting its own complicity. The Riksdag was convened to consider what to do.

The investigation that followed was not gentle to Johan Palmstruch. Royal commissioners examined the bank's books — what survived of them — and found inadequate records of issuance, missing copper, and loans extended without proper authorisation. Palmstruch was tried and convicted on charges that combined unauthorised issuance with insufficient bookkeeping. In 1668 he was sentenced to death. The sentence was commuted later that year to imprisonment, partly because Palmstruch's defenders argued, with considerable justice, that the over-issuance had been demanded by the very Crown now prosecuting him. He spent several years in prison before being released, and died in 1671 with his reputation in ruins.

The Riksens Ständers Bank: A Parliamentary Solution

The Riksdag of 1668 met in an atmosphere of broad consensus that something had gone badly wrong and that the answer was not to abandon paper banking but to reorganise it on different foundations. The four estates — nobles, clergy, burghers, and peasants — debated through the summer. The decision they reached was institutionally novel.

The new bank, chartered in September 1668, would not be a royal bank at all. It would be the bank of the Riksdag itself — owned, governed, and controlled by the four estates, with directors appointed by parliamentary committee and a charter that explicitly forbade the kind of Crown lending that had destroyed Palmstruch's institution. The bank was forbidden, in its early years, from issuing paper banknotes at all. The kreditivsedlar that had been the great innovation of Stockholms Banco were also the proximate cause of its ruin, and the Riksdag concluded that the experiment needed to wait until reserves and discipline could be guaranteed. Note issuance would not resume in earnest until the early eighteenth century.

The Riksens Ständers Bank opened for business in 1668 and absorbed what remained of Stockholms Banco's assets, taking responsibility for honouring its predecessor's notes — at a discount, but at a defined and orderly discount that allowed bondholders to recover something rather than nothing. This too was a deliberate departure from royal practice. The Crown might have repudiated the notes outright. The Riksdag chose to honour them, on terms that recognised both fiscal reality and the importance of preserving public trust in any future paper money.

Comparing the First Public Banks of the North

The Riksbank was not the first public bank in Northern Europe, nor even the first to issue paper instruments. It was, however, the first to be established under direct parliamentary authority — a constitutional design that explained both its survival and its eventual influence on later institutions, including the Bank of England.

| Bank | Founded | Sovereign | Innovation | Fate |

|---|---|---|---|---|

| Banco di Venezia | 1157 | Republic of Venice | Government debt market | Liquidated 1797 |

| Wisselbank (Amsterdam) | 1609 | City of Amsterdam | Bank money standard | Closed 1820 |

| Hamburg Bank | 1619 | City of Hamburg | Mark Banco unit | Closed 1875 |

| Stockholms Banco | 1656 | Swedish Crown | Printed banknotes | Failed 1668 |

| Riksens Ständers Bank | 1668 | Swedish Riksdag | Parliamentary control | Active (Riksbank) |

| Bank of England | 1694 | English Parliament | National debt funding | Active |

Each of these institutions solved a different problem. The Banco di Venezia created a market for government debt. The Wisselbank created a stable unit of account. Stockholms Banco created paper money. The Riksbank created the constitutional template — a public bank under legislative rather than executive authority — that would prove decisive when the Bank of England was founded twenty-six years later.

What the Riksbank Became

For the first century of its existence, the Riksbank operated as a relatively cautious deposit and lending institution. It resumed banknote issuance gradually, kept its reserves disciplined, and avoided the over-extension that had destroyed its predecessor. Its survival through the political turmoil of the early eighteenth century — including the calamitous reign of Charles XII, whose wars left Sweden bankrupt and whose mint master Baron Görtz issued debased emergency token coinage that wrecked Swedish credit — demonstrated the durability of parliamentary banking even when the broader fiscal regime collapsed.

The bank was renamed Sveriges Riksbank in 1867. Six years later, Sweden adopted the silver standard and joined the Scandinavian Monetary Union with Denmark and Norway. The krona, introduced in 1873 to replace the riksdaler, became the unit on which the Riksbank operated for the next century and a half. Sweden left the gold standard during the First World War, returned to it in 1924, and abandoned it for the last time in 1931 — earlier than Britain, partly because Riksbank officials had concluded earlier than their British counterparts that defending parity at any cost would do more damage than devaluation.

The Riksbank's most curious modern footprint is the Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel — established in 1968 to mark the bank's 300th anniversary, funded by the Riksbank, and administered by the Royal Swedish Academy of Sciences alongside the Nobel Prizes. It is, technically, not a Nobel Prize. It is, in practice, the closest thing to one that economics has, and the fact of its existence reflects the Riksbank's institutional confidence that it could comfortably mark its own tercentenary by funding a permanent international honour in monetary economics.

The Long Shadow

Goodhart, in his survey of central banking history, observed that "the truly remarkable feature of the Riksbank is not that it was founded earlier than other central banks, but that the constitutional principle on which it was founded — parliamentary rather than royal control of public money — turned out to be the principle that allowed central banks generally to survive the political upheavals of the modern age" (Goodhart, 1988). The English projectors who created the Bank of England in 1694 were aware of the Swedish precedent. So were the framers of the Federal Reserve in 1913, though by then the institutional landscape had grown so dense that direct lineage was impossible to trace.

What is undeniable is that the Riksbank still exists. Its premises in central Stockholm sit in a city now utterly unlike the seventeenth-century town in which Johan Palmstruch's depositors lined up for copper. The institution itself, however, traces an unbroken legal line back to that September day in 1668 when four estates of the Swedish Riksdag agreed that the experiment had to continue — but never again under the king alone.

The kreditivsedlar that Palmstruch printed are now museum pieces. The bank that learned from his failure prints — through its modern descendant, the Riksbank — the krona that Swedes still carry in their wallets. The line from Stockholms Banco to the Riksbank to every parliamentary central bank that has followed runs through one autumn afternoon in 1668, in a chamber in Stockholm where four estates of a parliament decided that public money was too important to leave to a king.

Related

Historical records Learn more about our methodology.