A Presidential War on a Bank

On 10 July 1832, Andrew Jackson sent Congress one of the most consequential veto messages in American history. The bill before him would have rechartered the Second Bank of the United States, the Philadelphia-headquartered institution run by Nicholas Biddle that held federal deposits, issued the country's most trusted paper currency, and acted as a rudimentary central bank. Jackson's message ran nearly seven thousand words. It called the Bank unconstitutional, in defiance of the Supreme Court's 1819 ruling in McCulloch v. Maryland. It called the Bank a tool of foreign shareholders, enumerating the 25 percent of its stock held in Britain and the Continent. And it called the Bank, in the line that became a slogan for a generation, "a monster" — an institution that, by virtue of its size and reach, was "hostile to the genius of our free institutions."

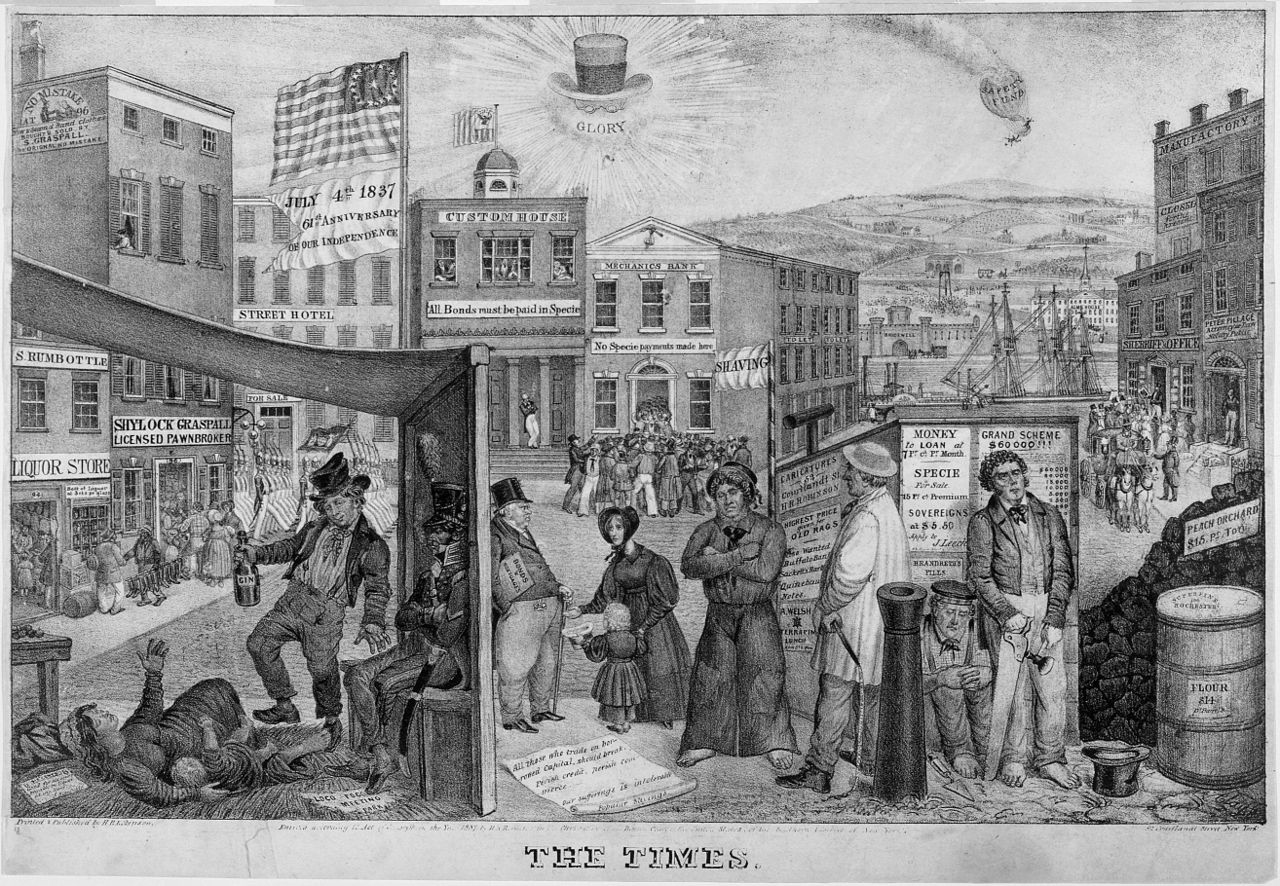

The veto held. Jackson won re-election that November on the slogan "Bank War," defeating Henry Clay, who had unwisely made the recharter his central campaign issue. What followed over the next five years was a sequence of policy decisions — some by Jackson, some by his Treasury secretaries, some by Congress, some by state legislatures, and some by foreign central banks — that produced the worst financial collapse the United States had yet seen. When New York City's banks suspended specie payment on 10 May 1837, the country entered a depression that would last six years, wipe out a third of commercial banks, default nine state governments, and leave America without a central bank until 1913.

Biddle's Bank and Its Enemies

The Second Bank of the United States had been chartered in 1816, a twenty-year franchise designed to bring monetary order after the chaos of War of 1812 finance. By the late 1820s, under Biddle's management, it had become a genuinely powerful institution. It held roughly $35 million in capital, maintained branches in 25 cities, and regulated state banks by refusing to accept their notes if those banks over-issued. Biddle understood this disciplinary function well. He wrote in 1828 that the Bank could act as "a check upon the state banks, to compel them to keep their issues within proper limits." To state bankers who resented the restraint, that check felt like tyranny.

Jackson came to the presidency in 1829 already hostile. A Tennessee man who had lost money in paper speculation before the war, he distrusted banknotes on principle. A states-rights Democrat, he distrusted any federal corporation. An anti-elitist populist, he distrusted Philadelphia's financial establishment most of all. His first annual message to Congress, in December 1829, questioned both the Bank's constitutionality and its effectiveness. Biddle, sensing a political opening, pushed for early recharter in 1832 rather than wait for the 1836 expiry. It was a strategic blunder that let Jackson build the veto into a re-election campaign.

Removal of Deposits and the Pet Banks

With the veto sustained and re-election secured, Jackson moved to strangle the Bank before its charter even expired. In September 1833, he ordered his Treasury secretary, William Duane, to withdraw federal deposits and place them with state-chartered banks. Duane refused; Jackson fired him. Roger Taney, later chief justice of the Supreme Court, took over the Treasury and executed the order. Federal revenues — chiefly from customs and public-land sales — began flowing into a rotating list of state banks that critics quickly dubbed the "pet banks." The initial list ran to 23 institutions; it grew to nearly 90 by 1836.

The pet banks had every incentive to lend aggressively. They received federal deposits for free, held no reserves against them beyond what prudence suggested, and competed against one another for Treasury patronage. Between 1833 and 1836, bank-issued notes in circulation nearly doubled, rising from about $61 million to $120 million. Specie reserves at banks rose too, buoyed by a surge in Mexican silver imports after the 1834 monetary reforms there, but they rose more slowly than note issue. The ratio of specie to liabilities fell. Biddle warned publicly that the country was "running a race of ruin." Few listened. Cotton was selling at seventeen cents a pound on the New Orleans wharves, and western land was changing hands at four and five times its 1831 value.

Source: Warren and Pearson wholesale price series, via US Historical Statistics

The British Rope

Behind the American cotton-and-land boom stood British capital. Baring Brothers, Rothschild, and a dozen smaller merchant houses financed American trade by accepting bills drawn on Liverpool cotton sales and discounting state bonds issued to fund canals and railroads. By 1836, foreign holdings of American securities had reached roughly $200 million — perhaps a quarter of the total stock of US debt and bank equity outstanding. The flow was sensitive to London interest rates, and London that autumn was tightening.

The Bank of England raised its discount rate from 4 to 4.5 percent in July 1836, then to 5 percent in September. The trigger was a gold drain caused in part by the same American boom — US importers and state governments drawing on London credits — and in part by bad harvests that pushed grain imports higher. The Bank of England also refused to rediscount bills drawn on seven Anglo-American merchant houses, the so-called "W banks" (Wiggin, Wilson, Wilde), throwing transatlantic trade credit into doubt. Jenks' classic study noted that British capital flows to the US peaked in 1836 and reversed sharply in the first half of 1837 (Jenks, The Migration of British Capital to 1875, 1927). Monthly data later pinned the bigger share of the 1837 collapse on the Bank of England's policy reversal rather than Jackson's Specie Circular, though the two shocks reinforced one another (Curott and Watts, 2018).

The Specie Circular

Jackson's final monetary intervention came on 11 July 1836. The Treasury issued a circular, drafted by the president's Kitchen Cabinet, that required federal land offices to accept only gold and silver — not banknotes — for public-land purchases of more than 320 acres. The intent, Jackson explained in his 1836 annual message, was to break "a spirit of speculation" and restore "a sound currency." The effect was the opposite of sound.

Speculators and farmers buying frontier land had to ship specie from eastern commercial centers to western land offices. Coin moved out of New York and Boston vaults, piled up in Illinois and Michigan land offices, and was sometimes lost in transit. Eastern banks saw reserves fall. At the same time, the federal government, flush with land-sale revenue, began distributing its surplus to state governments under the Deposit Act of June 1836 — another mandate that pulled specie from commercial banks. The Specie Circular's reserve impact was smaller than contemporaries claimed (Temin, 1969). A later monthly reconstruction disagreed, finding that the order's interaction with the Deposit Act's federal transfers was critical in draining New York vaults in the crucial spring of 1837 (Rousseau, 2002).

By early May, the New York City banks held roughly $1.5 million in specie against demand liabilities well over $25 million. On 4 May, the Dry Dock Bank failed. On 9 May, panic spread through Wall Street. On 10 May 1837, the directors of every commercial bank in New York City agreed to suspend specie payment. Philadelphia followed on the 11th. Baltimore and Boston followed within the week. Specie suspension — convertibility of paper to coin — was the nineteenth-century equivalent of a bank holiday. It did not close the banks; it only broke the gold promise.

| Year | Commercial banks in US | Banks failing that year |

|---|---|---|

| 1836 | 713 | 6 |

| 1837 | 788 | 343 |

| 1838 | 829 | 48 |

| 1839 | 840 | 93 |

| 1840 | 901 | 127 |

| 1841 | 784 | 107 |

| 1842 | 692 | 85 |

Van Buren and the Hard-Money Response

Jackson left office in March 1837, two months before the suspension. His successor, Martin Van Buren, inherited a country in free fall. Van Buren's response was to do almost nothing — in the first major depression of industrial America, the federal government declined to act as borrower, spender, or lender of last resort. "All communities are apt to look to government for too much," Van Buren told Congress in September 1837. "Especially at periods of sudden embarrassment and distress. But this ought not to be."

What he did propose was the Independent Treasury — a system under which federal funds would be held in government-operated sub-treasuries in specie rather than deposited with banks. The scheme passed in 1840, was repealed by the Whigs in 1841, and was restored by the Democrats in 1846. Its practical effect was to remove federal deposits from the banking system entirely, reinforcing the hard-money orthodoxy Jackson had begun. For the next 76 years, until the Federal Reserve Act of 1913, the United States had no central bank and no institutional lender of last resort. The Independent Treasury's rigidity worsened every subsequent panic by removing federal balances from commercial circulation precisely when liquidity was scarcest (Knodell, 2006).

The Second Suspension and State Defaults

The 1837 suspension lasted roughly a year; New York banks resumed specie payment in May 1838. Resumption proved premature. In October 1839, the Bank of the United States of Pennsylvania — Biddle's old institution, rechartered as a state bank after the federal charter lapsed — suspended again. Biddle had gambled on propping up the cotton price through the bank's own purchases, lost, and pulled his institution down with him. Philadelphia's suspension triggered a second wave of regional banking collapses across the south and west. Biddle himself was indicted for fraud in 1841; the charges were eventually dismissed, but his reputation did not recover before his death in 1844.

What followed was a cascade of state-government defaults. During the 1830s, states had borrowed aggressively in London to finance canals and railroads, pledging to service the debt from future toll revenue that never materialized. When markets closed, they could not refinance. Between 1841 and 1843, nine American states or territories repudiated or suspended payment on their bonds. British investors who had sold coal or cotton to Mississippi or Pennsylvania and taken state paper in return now held worthless securities. Reverend Sydney Smith's 1843 letter to the Morning Chronicle — "I never meet a Pennsylvanian at a London dinner without feeling a disposition to seize and divide him" — captured the English mood.

| State / Territory | Action | Year |

|---|---|---|

| Indiana | Suspension | 1841 |

| Illinois | Suspension | 1841 |

| Maryland | Suspension | 1841 |

| Michigan | Repudiation | 1842 |

| Pennsylvania | Suspension | 1842 |

| Arkansas | Repudiation | 1842 |

| Mississippi | Repudiation | 1842 |

| Louisiana | Suspension | 1843 |

| Florida Territory | Repudiation | 1843 |

Depth and Duration

How deep was the depression? The numbers rival the 1930s in some respects. Wholesale prices fell roughly 30 percent between 1837 and 1843. The money supply contracted about 34 percent between 1838 and 1843. Real GDP growth, hard to reconstruct for this era, appears to have been flat or negative for six consecutive years. Immigration slowed; western land sales collapsed from over 20 million acres in 1836 to fewer than 1.3 million in 1842. Cotton, which had peaked at 17.5 cents per pound in 1836, bottomed at 5.5 cents in 1844. Banks in states with the weakest reserve requirements — Michigan's free-banking law of 1837 produced dozens of "wildcat" banks, so named because they chartered branches in remote woods accessible only to wildcats — failed in waves.

Philip Hone, the former mayor of New York, kept one of the most vivid diaries of the period. On 11 May 1837, the day after the suspension, he wrote: "The fearful storm has burst upon the business community. The banks of New York have suspended specie payments." Six months later, he added: "The number of failures is so great daily that I do not keep the record of them." By the spring of 1842 he was recording suicides in his circle. Economic historians read these diaries alongside the macroeconomic data, and the combination is unmistakable. This was not a panic. This was a prolonged depression.

The Long Shadow: No Central Bank for 76 Years

The most lasting consequence of the Panic of 1837 was institutional. Jackson's victory over the Second Bank, cemented by Van Buren's Independent Treasury, meant that the United States would face every financial crisis between 1837 and 1913 without a central bank. The panics of 1857, 1873, 1884, 1893, and 1907 each unfolded in a monetary regime where the Treasury's only tools were the moral suasion of its clearing agents, the occasional bond issue, and direct calls on J.P. Morgan and other private financiers. The Panic of 1907 ended only when Morgan personally locked Trust Company presidents in his library until they agreed to a rescue fund. That episode, more than any other, finally convinced Congress that the American experiment in pure private central banking — the long Jacksonian inheritance — had to end, and the Federal Reserve Act of 1913 followed.

The contrast with Britain is sharp. When the Panic of 1825 nearly destroyed the Bank of England, Parliament strengthened the central bank rather than abolish it, giving it a note-issue monopoly in 1844 and letting Walter Bagehot codify the lender-of-last-resort doctrine in Lombard Street three decades later. The same Rothschild gold that saved Threadneedle Street in 1825 kept flowing into American state bonds in the 1830s, but without a Bank of England equivalent on the American side, the panic of 1837 had nowhere to land. Alexander Hamilton had argued exactly this case forty years earlier when he built the first Bank of the United States, writing that a national bank was "the dearest interest of the community." Jackson's veto, intended as a blow for democratic equality, ensured that for most of the nineteenth century the American financial system had no institution capable of halting a panic.

The Ledger

The Panic of 1837 was not one event but a three-act collapse — the May 1837 suspension, the October 1839 second suspension, and the state-default wave of 1841–1843 — that unfolded against a backdrop of aggressive British monetary tightening. Modern scholarship has moved away from the old Jacksonian-villain reading. International silver flows and Bank of England policy were the decisive drivers of the cycle (Temin, 1969). Modern time-series methods later confirmed and extended the result (Rousseau, 2002). The emphasis was pushed further toward London (Curott and Watts, 2018). None of this exonerates Jackson. The veto, the deposit removal, the pet-bank system, and the Specie Circular were each real policy errors that magnified the shock when it arrived. They also removed the one domestic institution that might have absorbed it.

Nicholas Biddle died a broken man in 1844, buried in Philadelphia's Christ Church cemetery with a plain stone. Jackson had died the year before, at the Hermitage, convinced he had saved the republic from financial despotism. Between their two graves lay six years of depression, 343 bank failures in a single year, nine bankrupt state governments, and the shape of an American financial system that would rely on Morgan's library and Rothschild's gold until a new generation of reformers built a central bank from scratch on Jekyll Island.

Related

Historical records Learn more about our methodology.