A Kingdom Drowning in Debt

By the summer of 1789, the Kingdom of France was functionally bankrupt. Louis XVI's government had inherited a debt burden stretching back decades, but the single largest accelerant was France's intervention in the American War of Independence. Between 1778 and 1783, France spent approximately 1.3 billion livres supporting the American rebels against Britain — a sum that swelled the royal debt to roughly 4 billion livres, with annual interest payments consuming more than half of government revenue (White, 1876). Jacques Necker, the Swiss-born finance minister, had papered over the deficit with borrowing, but by 1788 even that expedient had failed. Credit markets shut. Tax receipts fell short. Bread prices surged after a catastrophic harvest.

Louis convened the Estates-General in May 1789 — the first time in 175 years — not to reform the state but because he had no other way to raise money. Within weeks, the Third Estate declared itself the National Assembly, the Bastille fell, and the old fiscal order collapsed alongside the political one. Revolutionary France now faced a question that would define its monetary future: how to fund a new government when the treasury was empty and the tax system was in ruins.

Seizing the Church: Europe's Largest Asset Confiscation

On 2 November 1789, the National Assembly voted to place all Church property at the disposal of the nation. It was the largest asset seizure in European history. Ecclesiastical holdings — abbeys, farmland, urban properties, forests — amounted to an estimated 2 to 3 billion livres in value, roughly equal to the national debt itself (Sargent and Velde, 1995). In one stroke, the Revolution had acquired an enormous asset base. The problem was converting that illiquid real estate into immediate cash.

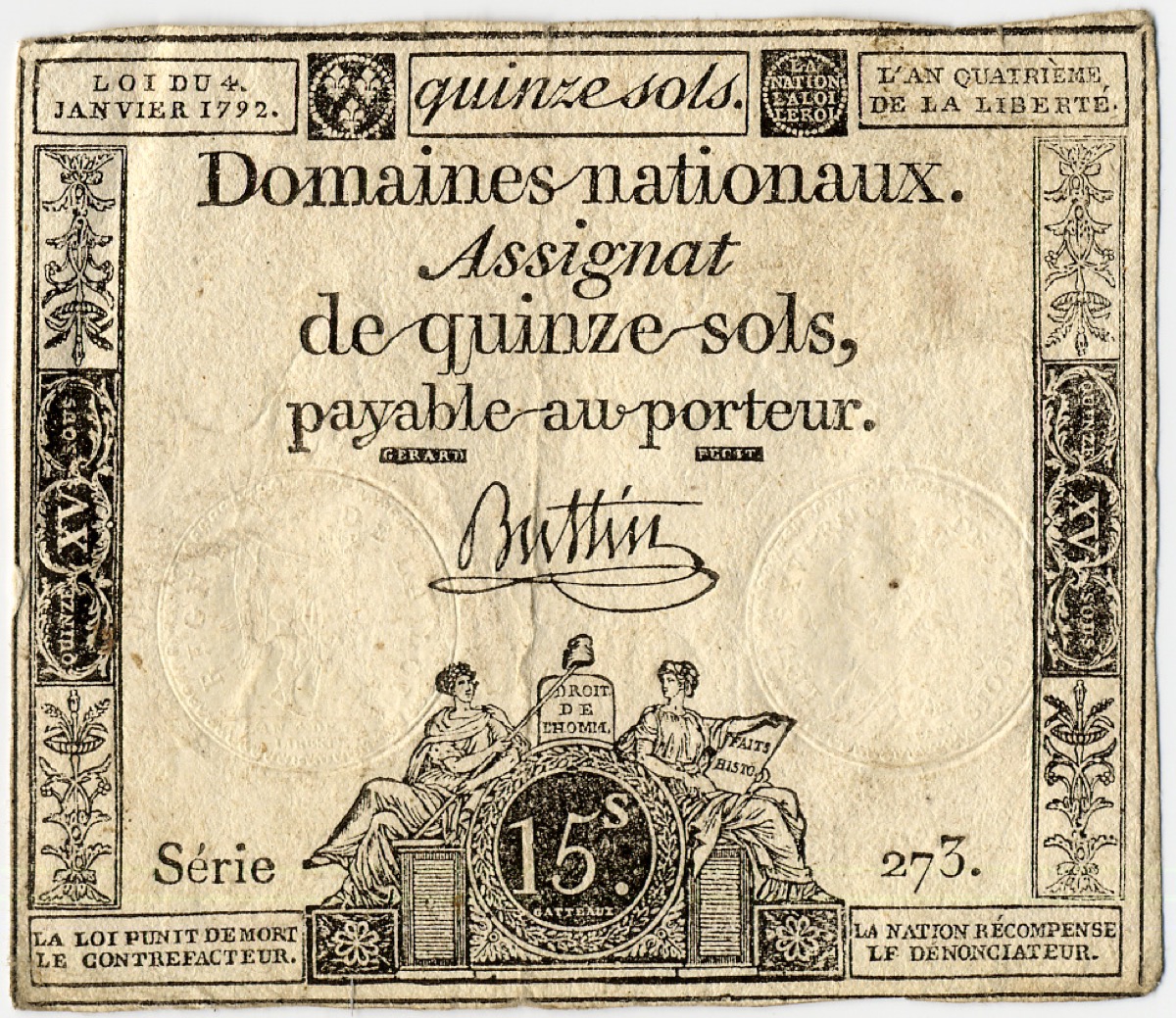

Charles-Maurice de Talleyrand, the Bishop of Autun, proposed the solution: issue paper notes backed by the confiscated lands. Holders could use these notes to purchase Church property at auction, and once the land was sold, the corresponding notes would be withdrawn from circulation and destroyed. It was an elegant mechanism — in theory. Paper backed by tangible assets, self-liquidating by design, a bridge between the old regime's debts and the new republic's land wealth.

In December 1789, the Assembly authorized the first issue of 400 million livres in assignats. They bore interest at 5 percent and came in large denominations — essentially government bonds rather than circulating money. No one imagined, at that moment, that these dignified instruments would become the most reviled currency in modern memory.

From Bond to Banknote: The Fatal Transformation

What happened next followed a logic that monetary historians would recognize in episode after episode, from John Law's banknotes in 1720 to Zimbabwe's trillion-dollar notes in 2008. A fiscal instrument designed for a specific, limited purpose was gradually transformed into general-purpose money — and then printed without limit.

In April 1790, the interest on assignats was abolished. In September, a second issue of 800 million livres was authorized, over fierce objections from Necker and the economist Pierre Samuel du Pont de Nemours. Comte de Mirabeau, the Revolution's most electrifying orator, led the charge for expansion. His argument was seductive: the lands backing the assignats were real, tangible, and vast. Why not unlock that wealth for the nation? Necker warned that once the printing press started, no assembly would ever vote to stop it. He was ignored.

By the end of 1790, assignats circulated as legal tender in denominations small enough for daily commerce. They were no longer bonds. They were money — and the government discovered what every government in fiscal distress eventually discovers: paper money is the easiest tax of all, requiring neither collectors nor consent.

The Ratchet: Print, Depreciate, Print Again

From 1791 onward, the dynamic became self-reinforcing. Revolutionary France faced simultaneous crises — war with Austria and Prussia beginning in April 1792, internal insurrection in the Vendee, bread shortages in Paris, the costs of mobilizing mass armies under the levee en masse. Each crisis demanded spending. Each round of spending required more assignats. Each new issue diluted the purchasing power of those already in circulation. Depreciation raised prices, which created the political demand for yet more printing.

Counterfeiting compounded the problem. British agents — and ordinary criminals — flooded France with forged assignats, which were relatively easy to replicate given the rudimentary printing technology of the era. Some historians estimate that counterfeit notes added as much as 30 to 40 percent to the effective money supply at various points (Harris, 1930). Revolutionary tribunals made counterfeiting a capital offense, but the guillotine proved no match for the printing press, whether official or illicit.

| Year | Cumulative Assignats Issued (livres) | Approximate Gold Value per 100 livres Face |

|---|---|---|

| 1789 | 400 million | 96 |

| 1790 | 1.2 billion | 95 |

| 1791 | 1.8 billion | 82 |

| 1792 | 3.4 billion | 57-72 |

| 1793 | 5.1 billion | 36-51 |

| 1794 | 8.0 billion | 31-34 |

| 1795 | 19.7 billion | 3-18 |

| 1796 | 45.0 billion | 0.5 |

The numbers tell the story with brutal clarity. Total issuance grew more than a hundredfold in seven years. Gold-equivalent value collapsed to near zero.

The Maximum and the Terror: Stabilization by Guillotine

By the summer of 1793, the Jacobin government under Maximilien Robespierre confronted an economy in free fall. Assignats had lost roughly two-thirds of their face value. Bread riots convulsed Paris. Hoarding was rampant — merchants who could see the trajectory of the currency refused to sell goods for paper, preferring to hold real commodities.

On 29 September 1793, the Convention enacted the General Maximum (Loi du Maximum General), imposing price ceilings on 39 essential commodities including bread, meat, firewood, and soap. Wages were capped at 50 percent above 1790 levels. Enforcement was severe: merchants who charged above the maximum faced fines, imprisonment, and — in the atmosphere of the Terror — the guillotine. Hoarding became a crime against the Republic. Citizens were encouraged to denounce neighbors who concealed grain or refused assignats.

For a brief period, the Maximum appeared to work. Prices stabilized. Assignat values even recovered modestly in early 1794, climbing from roughly 31 to 34 percent of face value. But the stabilization was an illusion maintained by fear. Farmers refused to bring produce to market at unprofitable fixed prices. Shops emptied. A thriving black market emerged where goods traded at their true prices — in metallic currency, not assignats. Goods available at the legal price simply disappeared; goods available at market prices could only be found in hidden transactions (Aftalion, 1990).

Robespierre understood that the assignat's value was inseparable from confidence in the Revolution itself. His speeches linked sound money to republican virtue, denouncing speculators and hoarders as enemies of the people. But virtue enforced by the guillotine could not repeal the laws of supply and demand. The Maximum distorted production, punished honest commerce, and drove economic activity underground.

Thermidor and the Inflationary Explosion

On 27 July 1794 — 9 Thermidor in the revolutionary calendar — Robespierre was overthrown and executed. With him went the Terror, and with the Terror went the only mechanism that had restrained the assignat's decline. The Thermidorian Convention, seeking to distance itself from Jacobin extremism, repealed the Maximum in December 1794.

What followed was monetary catastrophe. Freed from price controls, markets immediately repriced goods in line with the true quantity of paper in circulation. Assignat values, which had been artificially supported by the threat of execution, went into free fall. In January 1795, an assignat was worth roughly 18 percent of face value. By July, it had dropped to 3 percent. By February 1796, it traded at half of one percent — effectively worthless.

Daily life became a nightmare of depreciating currency. Workers demanded to be paid at the end of each day rather than the end of each week, racing to spend their wages before another day's depreciation consumed them. Restaurants posted prices in chalk, updated hourly. Peasants in the countryside reverted to barter, refusing paper entirely. Real estate speculation exploded as anyone with assignats sought to convert them into the one asset they were theoretically good for — confiscated Church lands. But even land auctions became chaotic, as the gap between the nominal and real value of assignats made rational pricing impossible.

Observers left vivid accounts. One Parisian diarist recorded paying 225 livres for a pound of sugar that had cost 1 livre five years earlier. A pair of shoes cost 2,000 livres. Fixed-income recipients — widows, pensioners, holders of government rentes — were reduced to penury. As in every hyperinflation, those who held real assets survived; those who trusted paper were destroyed.

The Mandats Territoriaux: A Second Failure

By early 1796, the Directory — the executive government that had replaced the Convention — recognized that the assignat was beyond salvation. On 19 February 1796, in a dramatic public ceremony on the Place Vendome, the government destroyed the assignat printing plates, the presses, and the paper stocks. It was a theatrical gesture meant to signal a new beginning.

In its place came the mandat territorial, introduced on 18 March 1796. Mandats were exchangeable at a fixed rate of 30 assignats to 1 mandat and could be used to purchase national lands directly at a stated price, without auction. The government hoped this would both replace the discredited assignats and accelerate the sale of remaining Church properties.

It did neither. Markets saw through the scheme instantly. Mandats began depreciating from the day of issue. Within five months they had lost 85 percent of their value. By August 1796, mandats traded at roughly the same contemptible fraction of par as the assignats they had replaced. On 4 February 1797, the Directory demonetized both assignats and mandats, effectively acknowledging that seven years of paper money had ended in total failure.

France limped through the remaining years of the Directory on a confused mixture of metallic currency, barter, and local credit arrangements. Specie — gold and silver coin — commanded enormous premiums. Commercial activity contracted sharply. The economy would not recover fully until a new political order brought a new monetary one.

Napoleon's Solution: Sound Money Through Authority

Napoleon Bonaparte, who seized power in the coup of 18 Brumaire (9 November 1799), understood that political legitimacy required monetary stability. On 18 January 1800, he established the Banque de France, granting it the privilege of note issuance under strict government oversight. Unlike the assignats, Banque de France notes were convertible into specie on demand.

In 1803, Napoleon introduced the franc germinal — named for the month Germinal in the revolutionary calendar — defined as 5 grams of silver or 290.322 milligrams of gold. This bimetallic franc would remain remarkably stable for more than a century, surviving revolutions, wars, and regime changes. It endured until 1914 without a single devaluation — one of the longest periods of monetary stability in modern history.

Napoleon's monetary settlement rested on three pillars: metallic backing that made overissuance mechanically difficult, institutional independence for the Banque de France (though Napoleon himself dominated it), and — critically — the memory of the assignats. French citizens had learned, at terrible cost, what unsecured paper could do. That memory was worth more than any gold reserve.

The Cautionary Tale That Never Died

In 1876, Andrew Dickson White — the co-founder of Cornell University — published Fiat Money Inflation in France, an essay that transformed the assignat from a historical episode into a permanent weapon in monetary debates. White meticulously traced the arc from the first reasonable issue through the inexorable expansion, the failed price controls, and the final collapse. His moral was explicit: paper money, once untethered from discipline, follows an inevitable trajectory toward worthlessness. The essay has been reprinted continuously for 150 years and remains a foundational text for hard-money advocates.

White's narrative drew heavily on the parallels with John Law's Mississippi scheme of 1716-1720, when France had suffered its first paper money catastrophe barely seven decades before the assignats. Law had created the Banque Generale, issued paper notes against the supposed wealth of Louisiana, and presided over a speculative mania that ended in the total repudiation of his currency. That France repeated the experiment so soon afterward — with so many of the same dynamics — struck White as evidence that nations learn nothing from monetary history.

The comparison cuts both ways. Law's scheme was a private venture wrapped in royal privilege; the assignats were a democratic experiment driven by genuine fiscal emergency. Law was a single visionary whose system collapsed when his personal authority wavered; the assignat was debased by successive governments, each facing pressures that made restraint politically impossible. But the endpoint was the same: paper money issued beyond the capacity of its backing, sustained by increasingly desperate coercion, collapsing once the coercion failed.

Legacy: Two Centuries of Monetary Conservatism

France's double experience with paper money — Law's notes in 1720, the assignats in 1796 — produced a monetary conservatism that persisted deep into the modern era. Throughout the nineteenth century, the Banque de France maintained a reputation for metallic orthodoxy. French investors preferred government rentes and gold hoarding to the kind of leveraged financial innovation that flourished in London and New York. When debates over bimetallism versus the gold standard convulsed Western economies in the 1870s and 1880s, France clung to its metallic anchor with particular tenacity.

This conservatism had real consequences. French banking remained relatively underdeveloped compared to Britain and Germany, partly because the cultural memory of paper money disaster made French savers deeply suspicious of bank-issued notes. Alexander Hamilton, building American credit in the same decade the assignats were collapsing, faced none of the visceral public hostility to public debt that paralyzed French fiscal policy for generations afterward.

The assignat also entered the intellectual toolkit of monetary economics. Alongside the Weimar hyperinflation and the various Latin American inflations of the twentieth century, it became a standard case study in textbooks on monetary theory. Economists from Irving Fisher to Milton Friedman cited the French experience as evidence that the quantity of money determines its value — the quantity theory in its starkest form.

Yet the assignat story is richer than the simple morality tale it is often reduced to. It demonstrates something subtler: that monetary instruments designed for one purpose — in this case, monetizing a legitimate asset base to solve a genuine fiscal crisis — can be corrupted beyond recognition when political incentives overwhelm institutional constraints. Every expansion of the assignat was, in isolation, defensible. France was at war. People were starving. The Republic faced existential threats. No single decision to print was irrational. But the cumulative effect of individually rational decisions was collective ruin.

That pattern — the ratchet, the emergency that justifies each new issue, the impossibility of reversal — is the deepest lesson of the assignat. It recurred in Weimar Germany, in post-war Hungary, in Argentina, and in Zimbabwe. It is not a lesson about the wickedness of governments or the folly of paper money. It is a lesson about the structural vulnerability of any monetary system in which the issuer of currency is also the entity with the most urgent need to spend it.

On the Place Vendome, where the Directory smashed the assignat presses in 1796, there is no plaque commemorating the event. But the ghost of that ceremony haunts every central bank charter that separates monetary authority from fiscal power — a separation that the men of 1789, for all their revolutionary genius, never thought to make.

Related

Historical records Learn more about our methodology.